Gujarat Board GSEB Textbook Solutions Class 11 Commerce Accounts Part 1 Chapter 1 Accounting and its Terminology Textbook Exercise Questions and Answers.

Gujarat Board Textbook Solutions Class 11 Accounts Part 1 Chapter 1 Accounting and its Terminology

GSEB Class 11 Accounts Accounting and its Terminology Text Book Questions and Answers

1. Write the correct option from those given below each question:

Question 1.

Under barter system, which of the following statement is not correct?

(a) Exchange of money for product

(b) Exchange of product for product

(c) Exchange of product for service

(d) Exchange of product/service for product/ service

Answer:

(a) Exchange of money for product

Question 2.

What is the limitation of accounting?

(a) Shows profitability

(b) Shows economic status

(c) Tax planning

(d) Stable value of money

Answer:

(d) Stable value of money

![]()

Question 3.

Accounting is known as ………………. .

(a) Historical accounting

(b) Future accounting

(c) Present accounting

(d) Unnecessary accounting

Answer:

(a) Historical accounting

2. Answer the following questions in one sentence:

Question 1.

Who provides capital to the business ?

Answer:

Owner provides capital to the business.

Question 2.

What is bad debt for business ?

Answer:

Bad debt is a loss for business. (It is not an expense of business.)

Question 3.

What is stable value of money ?

Answer:

Asset which was purchased in past, if the same asset can be purchased in future for reconstruct and its value is same, then it is called stable value of money. (Practically this is not possible.)

Question 4.

What is Double Entry System of accounting ?

Answer:

According to J. R. Batliboi : “Every business transaction has a two fold effect and that it affects two accounts in opposite directions and if a complete record is to be made of each such transaction it would been necessary to debit one account and credit another account. It is this recording of two fold effect of every transaction that has given rise to term Double Entry.”

Question 5.

State whether discount received is an income or expense ?

Answer:

Discount received is an income.

![]()

3. Answer the following questions in two or three sentences :

Question 1.

Explain Economic transaction.

Answer:

Economic transaction means a transaction which can be measured in terms of money. Business transactions are always economic transactions. Cash transaction, made in the form of money. Dues of credit transaction are receivable in future but its economic value is determined in present. Economic (Business) transaction comes into existence through medium of cash or on credit condition.

Question 2.

Describe types of liabilities.

Answer:

Liability can be classified into two categories : (1) On the basis of relation and (2) On the basis of time.

(1) There are two types of liabilities on the basis of relation : (i) Internal liability and (ii) External liability.

(2) There are two types of liabilities on the basis of time : (i) Current liability and (ii) Non-current liability.

Question 3.

Discuss types of assets.

Answer:

Types of assets are classified as under:

1. Non-current assets : Non-current assets are indentified on the basis of time. Assets, which are for the period of more than one year, means non¬current assets. They are also known as long-term assets or fixed assets. It can be categorized into two categories : (i) Tangible assets and (ii) Intangible assets.

2. Current assets : Current assets are those assets, whose time duration is of less than one year. These assets can be converted into cash. Cash and bank balance, debtors, bills receivable, raw material stock, finish stock, etc. are included in current assets.

3. Fictitious assets : Assets, which do not have physical form (existence), means fictitious assets. Realizable value of fictitious assets is zero. These assets are also known as spread revenue expenses or differed revenue expenses.

4. Real assets : Real assets means assets that have value in reality. From sales of such assets, if money can be realized, then they are known as real assets. These assets can be converted into cash.

Question 4.

Explain accounting as an art and a science.

Answer:

Accounting system is an art. Ability and skill are required to prepare the accounts within the limitations of accounting system. Properly written accounts are very important and useful for management.

Apart from art, accounting is known as a science also. Science is always based on rules and principles. Accounting is also written on certain rules and principles. Thus, due to rules and principles accounting is also known as science.

Question 5.

“Accounting is a language of business.” Explain.

Answer:

As in a language either by writing or speaking or analyzing or interpreting any content is described or explained by one person to other. Same function is performed by accounting, by providing information of business activities or results to the related parties. Just like as language, in accounting also time based changes are incorporated. Therefore, we can say that by giving information about accounts, accounting system works as a language.

![]()

Question 6.

Describe definition of accounting.

Answer:

American Institute of Certified Public Accounts (AICPA) has defined Accounting as follows :

“Accounting is an art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events, which are in part at least of a financial character and interpreting the results thereof.”

Definition is given by American Standards Council (ASC) as follows:

“It is a service activity. Its function is to provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making economic decisions.”

4. Answer the following questions in detail :

Question 1.

Explain Deshi Nama System and Double Entry System.

Answer:

There are two methods of accounting:

1. Deshi Nama Accounting System and

2. Double Entry Accounting System.

1. Deshi Nama Accounting System : Deshi Nama Accounting System is the ancient system of keeping accounts. This ancient system of Book keeping is still followed in India. This method is similar to Double Entry Accounting System, but it is structurally different from Double Entry Accounting System. Two important books are maintained under this method. Viz-‘Rojmel’ and ‘Khatavahi’. Rojmel is the basic book of accounts, which satisfies the requirement of cash book and journal. This system is also known as ‘Vahi (Bahi) Khata’ system.

2. Double Entry Accounting System: In

1494, an Italian mathematician Mr Luca Pacioli, presented firstly Double Entry Accounting System systematically. This method is widely used in India and in the other countries, as it is the most scientific method of accounting.

In Double Entry System of accounting, two effects of each transaction are recorded: They are namely: (i) Debit effect and (ii) Credit effect. Whatever amount is debited, same amount is credited. In every debit entry, we are able to get information of credit entry and in every credit entry, the information of debit entry is available. This is the peculatiry of this system and therefore this entry is known as Double Entry Accounting System. In the big business concerns and in companies, the accounts are prepared mostly by this method with the help of computer. This method is more scientific.

Question 2.

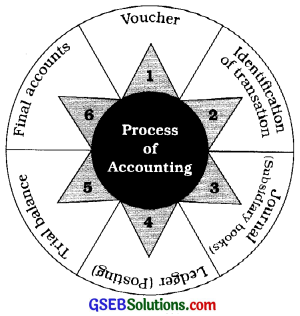

Explain process of accounting.

Answer:

Accounting system is a man made science, which has rules and principles. Accounts are prepared according to these rules and principles. The process of accounting is followed as under :

1. Voucher: While writing the accounts in the business, different bills, cash memo, receipts, counterfoil of the cheques, etc. are given. These kind of papers are called voucher. Business transactions are recorded in books of account on the strength of such vouchers. Voucher is an evidence supporting the transaction recorded in books of accounts. Voucher is the first step of a business transaction.

2. Identification of transaction: Identification of transaction is the second stage of the process of accounting. Here it is determined, whether the transaction of business is economic or noneconomic, whether the transaction is cash or credit or other transaction.

3. Journal (Subsidiary books) : Under the third stage of accounting process, economic transactions of business are recorded in journal or in subsidiary books.

4. Ledger (Posting) : Under the fourth stage, transaction recorded in journal or subsidiary books are classified through posting in a ledger. In short, posting will be made in the affected accounts from the journal or subsidiary books.

5. Trial balance: Under the fifth stage of accounting process, a trader prepares a statement from the balances of various accounts, which is known as a trial balance. Trial balance is the prior (first) stage of the preparation of final accounts.

6. Final accounts: Under the six and final stage of accounting process, Trading account, Profit and Loss account and Balance sheet are prepared on the base of trial balance and adjustments. It is called Final Accounts.

![]()

Question 3.

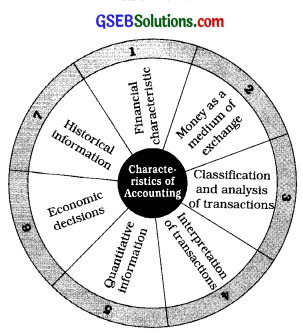

Discuss characteristics of accounting.

Answer:

Following are the characteristics of accounting:

1. Financial characteristic : Transactions or events, which are recorded in accounting, must be measurable in monetary value, e.g., 500 metre of clpth is purchased. This cloth is purchased for ₹ 50,000 which means that 500 metre cloth = ₹ 50,000. Rupee is money. Transaction made through money is known as economic transaction, which has financial characteristic.

2. Money as a medium of exchange:

Transactions or events recorded in accounting come into existence through the usage of money. Money as an exchange will be received by seller for 500 metre of cloth sold and by this money he can purchase any other product or service. In this manner money becomes medium of exchange for any transaction or event.

3. Classification and analysis of transactions : In a business different types of transactions take place like cash transactions, credit transactions or other special transactions, etc. These transactions are classified and analyzed on basis of their nature which is derived from debit-credit rules of accounting. Due to characteristic of classification and analysis, transactions of prescribed can be seen together at one place, e.g., What were opening balance of assets and debts? How many assets were purchased or sold? How many debts were taken or given ? What are closing balance of assets and debts ? Answers of all these questions are obtained because of classification and analysis.

4. Interpretation of transactions: Accounts are prepared according to specific rules and principles and then they are also interpreted on the basis of disclosed details and figures. Difference of expenses and incomes of a specific time duration decides profit or loss. With the interpretation of transactions results can be easily understood in accounting system.

5. Quantitative information : Quantitative information means numerical information. Information recorded in accounts is in the monetary form. So, this information is known as quantitative information.

6. Economic decisions : Different stakeholders take their decisions based on accounts prepared by accounting, e.g., Employees of a firm/company take decisions about salary, allowances, facilities on the basis of profit, while potential share-holders about investment, creditors about lending or selling take decisions and company itself makes decisions for its own development. Thus, accounting system is helpful to different parties to take economic decisions.

7. Historical information : The past always gives history. In accounting all past transactions and events are recorded. These past transactions or events become history. Past always discloses history. Accounts prepared on the basis of history represent historical information and results. Thus, accounting has relation with historical information.

![]()

Question 4.

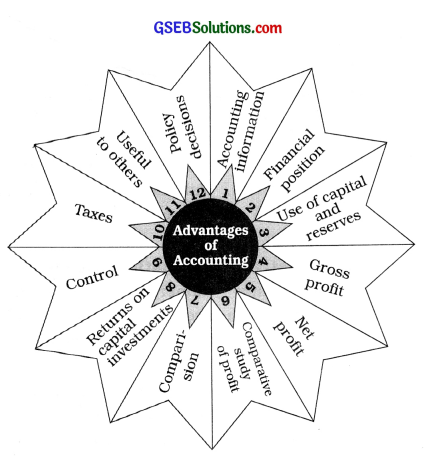

Describe advantages of accounting.

Answer:

By keeping books of accounts, financial position of the business can be known. There¬fore we can say that accounting is the image of business transactions. Various advantages or utilities of accounting are as under:

1. Accounting information: At the end of the specified period, receipts and payments as well as incomes and expenses of the business can be known. At the end of the year whether we have earned a profit or loss in the business can be known from final accounts prepared at the end of the year.

2. Financial position: At the end of specified period, information regarding business assets, liabilities, receivables, capital, etc. can be obtained.

3. Use of capital and reserves: From the financial position of the business we get the idea about how the capital, reserves, debts and annual profits are used in different goods – properties of the business.

4. Gross profit: At the end of specific period, from the information of purchases and sales, gross profit of the business can be known.

5. Net profit: At the end of specific period, from the information of gross profit and incomes- expenditures, we get the idea of net profit.

6. Comparative study of profit: Compare to the past years what is the change in the profit of current year, what are the reasons for that and what are the solutions for that, etc. can be decided.

7. Comparison : Book-keeping is useful for the comparison of accounts with the other business concerns and to take certain business decisions. For e.g., Advertisement expense.

8. Returns on capital investments : Returns on capital investments can be decided on the basis of profit. Comparative study of rate of capital investment is possible.

9. Control: Directly or indirectly informations are available which can throw some light on different malpractices done by employees and necessary steps can be taken to remove such unfair practices.

10. Taxes : It becomes easy to estimate the due government taxes like income tax, sales tax, VAT, octroi, etc.

11. Useful to others : With the help of books of accounts, insurance company, competitors, banks, employees, share-holders, creditors and government can obtain information regarding their interest and accordingly they can plan their strategy and can present their demands.

12. Policy decisions : With the help of book-keeping the development of business in the current year, compare to that of the previous year, can be known and depends on that which types of changes can be taken in the future that can also be decided.

Therefore, we can say that, accounting is a log chart of the past, a barometer of the present and a forecast of the future.

![]()

Question 5.

What are the limitations of accounting ?

Answer:

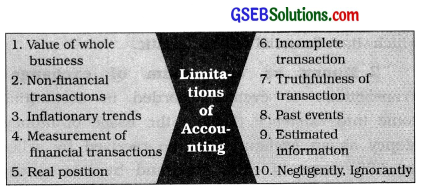

If the accounts are written systematically on the basis of accounting principles, it will bring many advantages. But if it is written negligently, without proper knowledge or if wrong entries are made intentionally, books of accounts will not show the true and fair financial position of the business. Limitations of accounting can be enumerated as under :

1. Value of whole business : Accounts do not reflect the exact value of the business as a whole,

because business is not evaluated on the basis of its assets and liabilities only, but it depends on other factors like place of the business in the s market, competitions, relations with employees,

monopoly, sale of goods, etc.

2. Non-financial transactions : Though non financial transactions are important from the view

point of the business, they are however not recorded in the books of accounts. For example, death of an efficient employee of the business.

3. Inflationary trends : In inflationary trends ? accounts do not reflect the true and fair financial position.

4. Measurement of financial transactions : On the basis of the assumption that value of money will be stable, all financial transactions are measured in terms of money only. It is not possible to record the transactions in the physical quantity. Hence, money is the common unit of measurement for all the transactions.

5. Real position : Fixed assets are shown at cost price less depreciation, but its market value may be different. Hence, accounts do not show the real position of the business.

6. Incomplete transaction : If the original transaction is incomplete or if it is not fully completed proper accounting record cannot be made. Because accounting is based on actual transactions.

7. Truthfulness of transaction : Accounting cannot provide protection against dishonesty or falsity of transaction. If transactions are not made, and fictitiously, if it is recorded by wrong vouchers, then accounts will not show true state of affairs.

8. Past events : Accounting provides information of the previous events. It does not show the information about the changes that are going to take place in the future for planning and controlling.

9. Estimated information : Many a times, accounting information is based on estimates. For example, depreciation, reserve for doubtful debts, discount reserve on debtors, value of closing stock, etc. These estimates can be inaccurate.

10. Negligently, Ignorantly : If entries are made negligently, fraudulently or ignorantly, it may adversly affect the business.

Besides the above limitations, it can be said that books of accounts provide useful information, as the above limitations are human created. Books of accounts can be checked by getting the accounts audited.

![]()

Question 6.

Who are the users of accounting information ?

Answer:

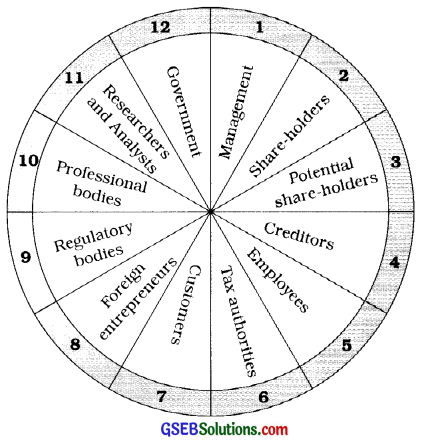

In a sole proprietorship firm or partnership firm accounts are kept for personal use of the owners or Government purposes. While in regard to the company due to Government restrictions details of company become public utility, i.e., usefulness of accounting to different parties can be explained as follows :

1. Management: The Board of Directors who are the elected representatives of the share-holders undertake the management of the company. The ethical (legal) decisions taken by these management people, effect on the profit and economic situation. Accounts are the greatest tools to know efficiency of the management. In short, Accounting is highly useful to management.

2. Share-holders : Because of legal provision of Company Act management has to send a true copy, of the company’s accounts in a stipulated time period to the share-holders. After studying

the report of accounts, the share-holders assess S about their investment in the company. Now all the companies have started sending report of s accounts to the share-holders by e-mail.

3. Potential share-holders : After studying the published report of accounts potential share-holders think about their possible benefits and then take decision of their investment.

4. Creditors : The short-term creditors take decision of giving credit by studying the published s accounts report of the company.

While long-term creditors can see possibility of investment.

5. Employees : The employees of the company get idea of salary, increment, bonus and other

facilities provided by the company. The progress l of a business unit shows safety of jobs, future salaries and compansations.

6. Tax authorities : State and Central Governments collect different kinds of taxes from the companies. The Tax Authorities get information about paid taxes and taxes according to budget from accounts report of the company.

7. Customers : The published accounts report of a company is very useful to the consumers (customers). Customer gets an idea about the company’s goods or services. The present market is of consumers only because consumer is the king of market.

8. Foreign entrepreneurs : Communication and transportation have brought the world closer and made it small. Liberalization has removed many economic restrictions. Hence to take the benifits many foreign companies wish to tie-up with domestic companies, therefore they need to study accounts details of the particular company.

9. Regulatory bodies : For safe guarding Common people from company’s in economic transactions the Government has set up two Regulator Bodies like SEBI and IRDA. These bodies require details of accounts for framing guidelines as well as rules and regulations.

10. Professional bodies : Those who maintain the accounts are known as Professional Bodies. Accounting system is a profession. Institute of Charatered Accountants, Institute of Charater Secretary and Institute of Cost Accounts of India give suggestions for uniform and equal maintence of accounts.

11. Researchers and Analysts : The researchers and analysts make study of company’s progress, profits, development and stability from the accounts report of the company.

12. Government: Government take proper decisions by collecting accounts details published by the company. Such kind of accounting information helps the Government to fram economic laws of the nation.

![]()

Question 7.

Explain the qualitative characteristics of accounting.

Answer:

Qualitative characteristics of accounting information prove helpful to the user and also help him take various decisions. Following are the qualitative characteristics of accounting information :

1. Understandability : Accounting information should be presented in such a manner that the user can understand it easily. The accounting information should be presented appropriately and accurately. For example, if an entry is recorded for a transaction which is not properly classified or if its language is ambiguous or not clear it would not be possible to understand the accounting statements properly.

2. Relevance : Accounting information should have the quality of relevance. The accounts should be prepared and presented keeping in view of the objectives. In the context of such objectives, the accounts should comprise all necessary information. Accounting statement prepared at the end of accounting period should satisfy the required objective. For example, the person who is giving away loan would require (be interested) to know whether the assets are free of charge ? Whether such assets are recorded at their proper values?

3. Reliability : Accounting information should be authentic and reliable. That is, it should not contain any error or false presentation. While writing the accounts the biased view should not be adopted and such accounts should be presented in a neutral manner.

4. Comparability : The quality of comparability needs to be followed while writing the accounts. Hence accounting information of a firm should be comparable for different years. Likewise accounting information of various firms should be comparable for any particular year. Therefore, the accounting statements of any company shows the figures of previous year as well as for current year. Accounts should be written as per those accounting principles which are generally accepted by all.

Question 8.

Explain the following technical terms :

1. Capital and Drawings

Answer:

Capital: The amount invested in the business by the proprietor, to run the business is known as capital. Amount brought in the business in this way may be in form of cash, goods or assets. In short, consideration given to the business by owner means capital. As the proprietor is the giver of consideration, the amount will be credited to the capital account of proprietor. On the profit or loss, right of the proprietor is there and therefore, if profit is there capital increases and if loss incurred capital decreases. In other meaning or way, capital means, excess of assets over liabilities. Capital = Assets – Liabilities.

Capital is identified on basis of nature of business, which is as follows :

- For sole proprietorship capital word is used, which owner provides.

- For partnership, partners’ capital word is used, which partners provide.

- For company, share capital word is used, which Is providesd by share-holders.

Drawings: If the owner of the business has taken away any amount of cash, goods, assets or services, for personal use, the amount so withdrawn is known as drawings. Drawing account will be opened to record the different transactions of the drawings which take place during the accounting year. Drawing account is personal account in nature. Capital will be reduced by the amount of drawings. At the end of the accounting year, drawing account is transferred to capital account, that means amount of drawing is deducted from the capital amount.

2. Capital receipts and Revenue receipts

Answer:

Capital receipts : The receipts received on sale of assets or the receipts are obtained by any long-term debt, are known as capital receipts, e.g., Income from sale of old machinery, amount received on issuing debentures, etc. Capital receipts are not received regularly and frequently. Such receipts are credited to special fund or capital fund.

Revenue receipts: Receipts received from the day-to-day transactions of the business are known as revenue receipts, e.g., brokerage received, interest received, amount received on the sale of goods, etc. The flow of these receipts would remain constant. From these receipts profit earned during the year or loss incurred can be ascertained. Such receipts are received regularly and frequently. In short routine receipts of the business are known as revenue receipts or incomes.

![]()

3. Payables and Receivables

Answer:

Payables: Any amount to be paid by the businessman in the future to any person or persons is known as payables, e.g., creditors, bills payable, outstanding expenses, pre-received incomes, etc. are included in payables. All these payables are considered as liabilities. There are two types of liabilities : (1) Current liability and (2) Long-term liability.

Receivables: Any amount to be received by the businessman in the future from any person or persons is known as receivables, e.g., Debtors, bills receivable, outstanding incomes, prepaid expenses, etc. are included in receivables. All these receivables are current assets.

4. Debit and Credit

Answer:

Debit and credit are two important words of accounting:

Debit: In Double Entry System the left hand side of an account is known as debit side. The process of writing an amount on the debit side of an account (L.H.S. of writer) with necessary particulars is known as debiting the account. The name of account credited should be written in the column of particulars.

Credit: In Double Entry System the right hand side of an account is known as credit side. The process of writing an amount on the credit side of an account (R.H.S. of writer) with necessary particulars in known as crediting the account. The name of account debited should be written in the column of particulars.

5. Account

Answer:

Account means a systematic accounting summary which shows the transactions of specific period for goods, assets, persons, incomes and expenses. In the account, any one effect of transaction – debit or credit-is passed. Moreover to find the difference between the totals of both the sides, which is also known as balance of that account, is also included.

Illustration: In each transaction minimum two accounts are effected, e.g., Goods of ₹ 9,000 sold to Manas for cash. Here two accounts are effected : (1) Cash account and (2) Goods (Sales) account.

In short, to distinguish some specific class of transactions from other transactions of business, a systematic summary of the same is prepared which is known as an account.

6. Voucher

Answer:

A documentary or written evidence of the transactions of the business is known as voucher. Since such evidence is in the written form, it could be preserved for a very long time. Moreover, it could be produced as a proof at a future date, when required. Bill or invoice (cash memo) for cash purchase, bill (credit memo) for credit purchase, credit note, debit note, counter foil of cheque, pay-in slip for cash deposited in the bank, receipt issued or received, etc. are the examples of the voucher.

Business transactions are recorded in books of account on the strength of such vouchers only. Vouchers also help to ensure that an accounting entry passed is true and correct, e.g., Invoice issued by a seller is the basis of accounting entry for recording purchase in Purchase Book. Similarly, office copy of the sales invoice is the basis for recording sales.

![]()

Question 9.

Explain the methods of maintaining accounts on Mercantile System and Cash System (Basis).

Answer:

To prepare accounts under Double Entry System, three different bases are used : 1. Mercantile base, 2. Cash base and 3. Mixed base.

1. Mercantile base : In this system accounts are written according to the accounting year. When accounts are prepared under this method, following points must be remembered :

- All transaction of that respective year are considered.

- Incomes are recorded as and when they accrues or earned and expenses are recorded as and when they are due or become payable.

- Both the types of transactions viz. cash transactions and credit transactions are recorded.

- Cash incomes and expenses related transactions of previous year or next year are not considered to determine profit/loss.

- The transactions of the previous year are recorded in the previous year and the transactions of the next year will be recorded in the next.

- In transactions of that accounting year, transactions pertaining to receipts, payments, liabilities and assets are included.

- Incomes and expenses of respective accounting year are consider. Where outstanding incomes, expenses paid in advance, expenses outstanding, incomes received in advance, etc. are included.

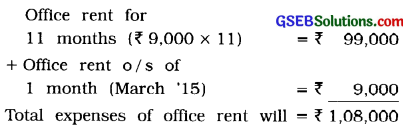

In short, under this system a record is made on the basis of amounts having become due for receipt and payment. - Illustration: Assume that accounts are prepared for the period 1-4-T4 to 31-3-T5 and office rent of ₹ 9,000 is paid every month. Further assume that office rent of March T5 is outstanding. It will be recorded as under :

be considered in current accounting year.

This is a very popular method. In practice, excluding certain sectors, in all the other sectors, the accounts are maintained under mercantile system. This system is also known as Accrual base of accounting.

2. Cash base: Professional persons like Doctors, Lawyers, Chartered Accountants, etc. can keep record of their accounts under this method. The use of this method is very limited. When accounts are prepared under this method, following points must be remembered :

- Only all cash transactions of that respective accounting year are recorded.

- Credit transactions as well as barter transactions are not recorded.

- Cash transactions of that respective accounting year include transactions pertaining to receipts, payments, liabilities and assets.

- The cash transaction of the previous year, the current year and the next year are also considered.

- Every transaction in which cash comes into the business or cash goes out of the business is . recorded with its specific purpose.