Gujarat Board GSEB Class 11 Commerce Accounts Important Questions Part 2 Chapter 9 Accounts of Non-trading Concerns Important Questions and Answers.

GSEB Class 11 Accounts Important Questions Part 2 Chapter 9 Accounts of Non-trading Concerns

Answer the following questions in one sentence :

Question 1.

Why does a non-trading concern prepare its accounts?

Answer:

A non-trading concern prepares its accounts to provide information to its members regarding the receivables and payable and if possible to obtain grant (Subsidy) from the government.

Question 2.

What is revenue expense?

Answer:

Expense which is incurred to carry on day-to-day activities of an institution, to maintain the assets in proper and efficient condition or the expense whose benefit is going to be received by the institution for the current year only is known as revenue expense.

Question 3.

What is revenue income?

Answer:

The income received from the regular activities of the institution is known as revenue income.

Question 4.

What is capital income?

Answer:

The income of a concern which is not regular in nature, as well as the benefit of which income is available for a longer period of time is known as the capital income.

![]()

Question 5.

Explain: Capital fund OR Permanent fund.

Answer:

Capital fund can be compared with the capital of a trading concern; Except the funds received for specific purpose, all capital income received or amounts capitalised are shown under this head.

Question 6.

The Receipts and Payments Account is similar to which acccount?

Answer:

The Receipts and Payments Account is similar to Cash Account (cashbook).

Question 7.

The Income and Expenditure Account is similar to which account?

Answer:

The Income and Expenditure Account is similar to the Profit and Loss Account of trading concerns.

Question 8.

What is main motive of Non-Trading Conems ?

Answer:

The main motive of Non-Trading Concerns, is not to earn profit but to render services.

Question 9.

What is deferred revenue expenditure ?-

Answer:

Expenditure which is basically revenue expenditure but benefits of which accrued to the concerns for more than a year is called deferred revenue expenditure.

Question 10.

Give three examples of deferred revenue expenditure.

Answer:

Following are the three examples of deferred revenue expenditure :

- Preliminary expenses,

- Advertisement campaign expenses on large scale and

- Expenses for issue of shares or debentures.

![]()

Question 11.

What do you mean by recurring expenses?

Answer:

Recurring expenditure is that expenditure of which benefit lasts for a maximum period of one year and is incurred on purchase of goods or services, in order to carry out the main activity of the concern.

Question 12.

What does ‘Surplus’ mean?

Answer:

Excess of income over expenditure shown by Income and Expenditure Account represents surplus for the accounting year.

Question 13.

What do you mean by subscription?

Answer:

Subscription is the periodical payment made by the members to the Non-Trading Concerns for maintaining his membership.

Question 14.

What is an entrance fee?

Answer:

The fees paid by the persons who wish to become a member of the organisation are called entrance fees.

Question 15.

What is ‘deficit’?

Answer:

Excess of expenditure over income shown by Income and Expenditure Account represents deficit for the accounting year.

Question 16.

What do you mean by non-recurring expenses?

Answer:

Non-recurring expenditure is any capital expenditure which is spent for acquisition of fixed assets like purchase of land or furniture, in order to run the concern and it gives benefits for a long period say more than three years.

![]()

Question 17.

Which ‘Final Accounts’ do the Non-Trading Concerns prepare?

Answer:

The Non-Trading Concerns prepare Income and Expenditure Account and Balance Sheet in their final accounts.

Question 18.

Which account is prepared by the Non-Trading Concerns for finding out Surplus or Deficit of the financial year?

Answer:

Income and Expenditure Account is prepared by the Non-Trading Concerns to find out Surplus or Deficit of the financial year.

Question 19.

Which account does Non-Trading Concerns prepare instead of Cash Account/Bank Account?

Answer:

Non-Trading Concerns prepare ‘Receipts and Payments Account instead of Cash Account/Bank Account.

Question 20.

Which capital incomes are disclosed separately in the Balance Sheet?

Answer:

The Prize fund, Construction fund, President felicitation fund, Donation received for tournament fund, etc. are disclosed separately at the liability side of the Balance Sheet.

Question 21.

Where is revenue income disclosed?

Answer:

Revenue income is disclosed on the credit side of the Income and Expenditure Account.

Question 22.

By which other name deferred revenue expenses is known?

Answer:

Deferred revenue expense is also known as spread expense.

Question 23.

Where is the portion of deferred revenue expense disclosed?

Answer:

The portion of deferred revenue expense is disclosed on the asset side at the end of the Balance Sheet.

![]()

Question 24.

By which other name is Capital fund known?

Answer:

Capital fund is also known as Permanent Fund.

Question 25.

How will you treat excess of income over expenditure?

Answer:

Excess of income over expenditure is added to the capital fund on the liability side of a Balance Sheet.

Question 26.

Where are capital expenditures recorded?

Answer:

Capital expenditures are recorded on the asset side of Balance Sheet.

Question 27.

Where are revenue expenditures shown?

Answer:

Revenue expenditures are shown on the debit side of Income-Expenditure Account.

Question 28.

Which entries are not to be included in Receipts and Payments Account?

Answer:

Credit transactions entries and adjustments entries are not to be included in Receipts and Payments Account.

Question 29.

Why is Receipts and Payments Account prepared?

Answer:

As to know about the cash receipts and payments transactions during a year in Non¬Trading Concerns, Receipts and Payments Account is prepared.

![]()

Question 30.

How many types of expenses are there in Non-Trading Concerns? Which are they?

Answer:

Non-Trading Concerns have three types of expenses :

- Capital expenses,

- Revenue expenses and

- Deferred revenue expenses.

Answer the following questions as asked :

Question 1.

Classify the following as Revenue income, Capital income, Revenue expense and Capital expense:

1. Income from lectures

2. Purchase of Story and Novel books for library

3. Sale of old magazines and newspapers

4. Prize fund

5. Donation for books

6. Poet conference expenses

7. Income of poet’s conference

8. Repairing expenses

9. Wages for installation of furniture

Answer:

| Revenue income | Capital income | Revenue expense | Capital expense |

| 1. Income from lectures

3. Sale of old magazines and newspapers |

4. Prize fund

5. Donation for books |

6. Poet conference expenses

8. Repairing expenses |

2. Purchase of Story and Novel books for library

9. Wages for installation of furniture |

Question 2.

Classify the following as Capital income, Revenue income, Capital expense and Revenue expense:

1. Income from entertainment programme 2. Expenses of charity show 3. Tournament expenses 4. Electrical fittings 5. Charity 6. Sale of sports equipment 7. Purchase of sports equipments

8. President’s felicitation fund 9. Annual function expeneses 10. Rent of hall 11. Sonography machine 12. Donation received for pavillion

Answer:

| Capital income | Revenue income | Capital expense | Revenue expense |

| 5. Charity 8. President’s felicitation fund 12. Donation received for pavilion |

1. Income from entertainment programme

6. Sale of sports equipments 10. Rent of hall |

4. Electrical fittings

7. Purchase of sports equipments 11. Sonography machine |

2. Expenses of charity show

3. Tournament expenses 9. Annual function expense |

Question 3.

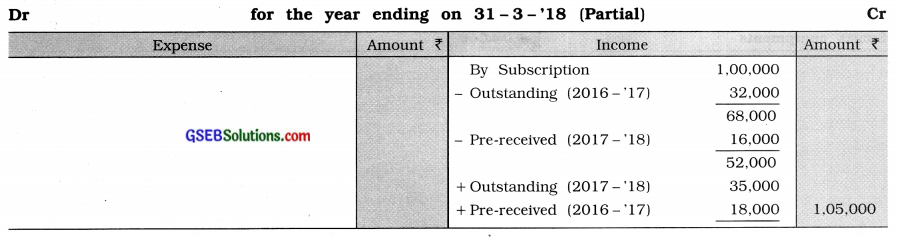

Show the following information in the Income-Expenditure Account ending on 31-3-’18 and Balance Sheet as of that day. Subscription received in the year 2017-’18 is ₹ 1,00,000.

| Particulars | Amount ₹ on 1-4-’17 | Amount ₹ on 31 – 3 – ’18 |

| Outstanding Subscription | 32,000 | 35,000 |

| Pre-received Subscription | 18,000 | 16,000 |

Answer:

Income-Expenditure Account

Balance Sheet as on 31-3-’18 (Partial)

| Liabilities | Amount ₹ | Assets | Amount ₹ |

| Pre-received Subscription | 16,000 | Outstanding Subscription | 35,000 |

![]()

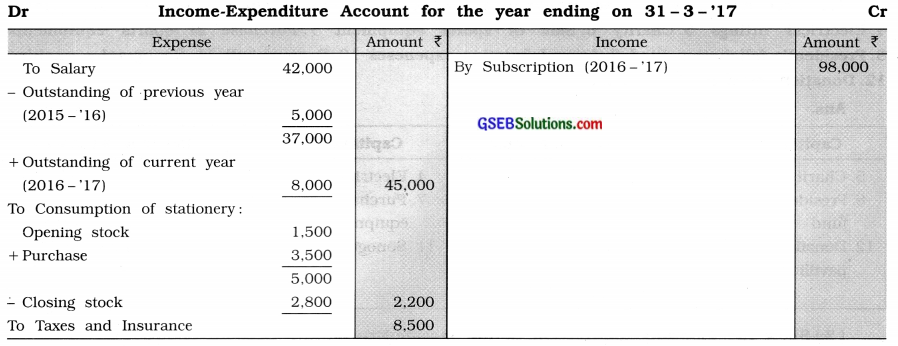

Question 4.

Show the following particulars in the Income and Expenditure Account for the year ended on 31-3-’17:

Note: 1. Salary outstanding 2015 – ’16: ₹ 5,000;

2016-’17: ₹ 8,000

2. Opening stock of stationery ₹ 1,500 and Closing stock of stationery ₹ 2,800

Answer:

Question 5.

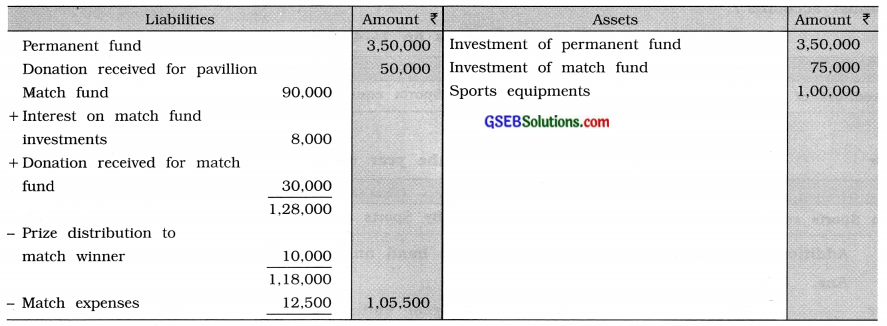

Record the following balances in the Balance Sheet of Rajpath Cricket Club:

| Balances of Accounts | Amount ₹ | Balances of Accounts | Amount ₹ |

| Permanent fund | 3,50,000 | Investments of match fund | 75,000 |

| Investment of permanent fund | 3,50,000 | Interest on match fund investments | 8,000 |

| Match fund | 90,000 | Donation received for match fund | 30,000 |

| Match expenses | 12,500 | Donation received for pavillion | 50,000 |

| Prize distribution to match winners | 10,000 | Sports equipments | 1,00,000 |

Answer:

Balance Sheet of Rajpath Cricket Club as en … (Partial)

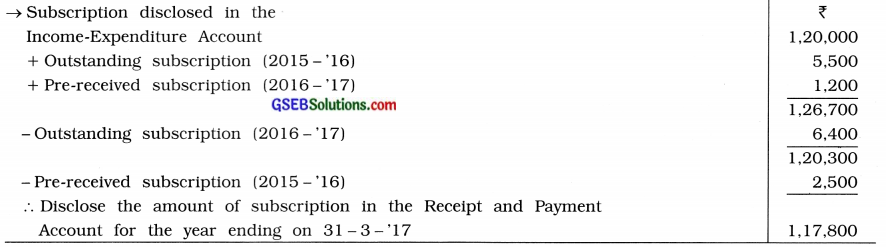

Question 6.

Income of subscription ₹ 1,20,000 is disclosed in the Income-Expenditure Account for the year ending on 31-03-’17. Other details of subscription are as follows:

| Particulars | Amount ₹ on 31 – 3 – ’16 | Amount ₹ on 31 – 3 – ’17 |

| Outstanding Subscription | 5,500 | 6,400 |

| Pre-received Subscription | 2,500 | 1,200 |

Show the amount of subscription in the Receipt and Payment Account for the year ending on 31-03-’17.

Answer:

Only subscription received by cash is shown in Receipt and Payment Account while total subscription of the current year is shown in Income-Expenditure Account.

Explanation: Given reverse effect of subscription of Income and Expenditure Account, forgetting the amount of subscription as per Receipt-Payment Account.

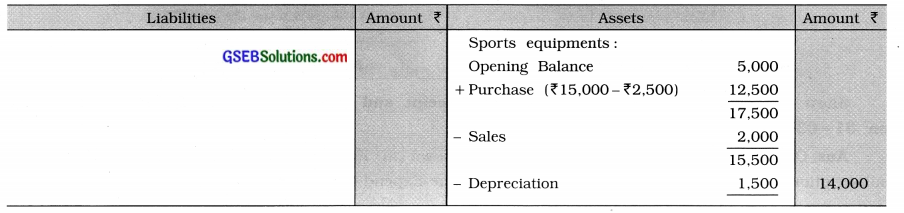

Question 7.

How would you disclose the following details on 31-03-’17, during the preparation of annual accounts?

Balance Sheet as on 1-4-’16

| Liabilities | Amount ₹ | Assets | Amount ₹ |

| Creditors of sports equipments | 2,500 | Sports equipments | 5,000 |

Additional information: Sports equipment on hand on 31-3-’17 ₹ 14,000

Answer:

Balance Sheet as on 31-3-’16 (Partial)

Explanation : Depreciation on sports equipments

= Opening Balance + Purchase – (Sales + Closing Stock) = 5,000 + 12,500-(2,000 + 14,000)

= 17,500-16,000 = ₹ 1,500

Write the correct option from those given below each question :

Question 1.

What kind of expense, an expense incurred to increase efficiency of business assets is?

(a) Revenue

(b) Capital

(c) Deferred revenue

(d) Sundry

Answer:

(b) Capital

Question 2.

The income which is received regularly and which arises from the routine activities of an institution is known as ……………….. .

(a) Sundry income

(b) Capital income

(c) Revenue income

(d) Personal income

Answer:

(c) Revenue income

![]()

Question 3.

From the following, which expense is deferred revenue expenditure?

(a) Sale of old newspapers

(b) Colourwork expense of new building

(c) Expenses of annual gathering function

(d) Expenses for issue of shares or debentures

Answer:

(d) Expenses for issue of shares debentures

Question 4.

From the following, which is not capital income?

(a) Donations

(b) Charity

(c) Govt, grant

(d) Legacy

Answer:

(c) Govt, grant

Question 5.

How many methods are there to maintain accounts of Non-Trading Concerns?

(a) Two

(b) Three

(c) Four

(d) Five

Answer:

(a) Two

Question 6.

By which name the capital of Non-Trading Concerns is known?

(a) Fixed capital

(b) Capital reserve

(c) Permanent fund

(d) Reserve fund

Answer:

(c) Permanent fund

Question 7.

Which is the main income of Non-Trading Concerns?

(a) Donation

(b) Government aid

(c) Legacy

(d) Subscription of members

Answer:

(d) Subscription of members

Question 8.

What is Life Membership Fee for the Non-Trading Concerns?

(a) Revenue income

(b) Capital income

(c) Revenue expense

(d) Capital expense

Answer:

(b) Capital income

![]()

Question 9.

What is ‘machine installation wages’ for the Non-Trading Concerns?

(a) Capital income

(b) Capital expense

(c) Revenue income

(d) Revenue expense

Answer:

(b) Capital expense

Question 10.

From the following, which is capital income?

(a) Entrance fee

(b) Prize fund

(c) Membership fee

(d) Govt. Subsidy

Answer:

(b) Prize fund

Question 11.

From the following, which is revenue expense?

(a) Purchase of billiard table

(b) Expense to bring an old asset in operation

(c) Machine installation expense

(d) Repairing expense of machine

Answer:

(d) Repairing expense of machine

Question 12.

Which type of Receipt and Payment Account is?

(a) Personal Account

(b) Real Account

(c) Nominal Account

(d) Profit and Loss Account

Answer:

(b) Real Account

Question 13.

Excess of Expenditure over Income is termed as …………………………… .

(a) Surplus

(b) Deficit

(c) Capital fund

(d) Profit

Answer:

(b) Deficit

Question 14.

A donation received for a specific purpose is a ……………………. .

(a) Capital receipt

(b) Revenue receipt

(c) Liability

(d) Asset

Answer:

(a) Capital receipt

![]()

Question 15.

Which account is prepared instead of Profit and Loss Account in Non-Trading Concerns?

(a) Trading account

(b) Cash account

(c) Income and Expenditure account

(d) Receipts and Payments account

Answer:

(c) Income and Expenditure account

Question 16.

Which type of Income and Expenditure Account is?

(a) Capital account

(b) Real account

(c) Personal account

(d) Nominal account

Answer:

(d) Nominal account

Question 17.

Excess of Income over Expenditure is termed as ……………………….. .

(a) Deficit

(b) Profit

(c) Surplus

(d) Loss

Answer:

(c) Surplus

Question 18.

Only which incomes and expenses are shown in the Income and Expenditure Account?

(a) Revenue

(b) Capital

(c) Business

(d) Non-recurring

Answer:

(a) Revenue

Question 19.

From the following, which is Non-Trading Concerns?

(a) Mehta hospital

(b) Gujarat hospital

(c) Vadilal Sarabhai hospital

(d) Siddi-Vinayak hospital

Answer:

(c) Vadilal Sarabhai hospital

Question 20.

What is the main objective of a Non-Trading Concern?

(a) To earn profit

(b) To provide services

(c) To receive legacy

(d) To provide charity

Answer:

(b) To provide services

![]()

Question 21.

What is a Receipt-Payment Account similar to?

(a) Cashbook

(b) Bankbook

(c) Ledger book

(d) Journal book

Answer:

(a) Cashbook

Question 22.

What is Income and Expenditure Account similar to?

(a) Trading Account

(b) Profit and Loss Appropriation Account

(c) Profit and Loss Account

(d) Revaluation Account

Answer:

(c) Profit and Loss Account

Question 23.

What is credit balance of Income and Expenditure Account called?

(a) Excess of income over expenditure

(b) Excess of expenditure over income

(c) Net profit

(d) Net loss

Answer:

(a) Excess of income over expenditure

Question 24.

Where are capital income expenses shown?

(a) In Profit and Loss A/c

(b) In Income and Expenditure A/c

(c) In Receipt-Payment A/c

(d) In Balance Sheet

Answer:

(d) In Balance Sheet

Question 25.

Which transactions are not recorded in Receipts-Payments Account ?

(a) Cash received transactions

(b) Cash payment transactions

(c) All types of bank transactions

(d) Non-cash transactions

Answer:

(d) Non-cash transactions

![]()

Question 26.

What is called credit balance of Receipts- Payments Account?

(a) Bank balance

(b) Cash balance

(c) Bank overdraft

(d) Bank loan

Answer:

(c) Bank overdraft

Question 27.

In which year income received and amount paid are recorded in Receipt-Payments Account?

(a) Current year

(b) Previous year

(c) Next year

(d) Any year

Answer:

(d) Any year

Question 28.

Where are non-cash items not recorded from the following?

(a) Income and Expenditure Account

(b) Receipts and Payments Account

(c) Balance Sheet

(d) Profit and Loss Account

Answer:

(b) Receipts and Payments Account

Question 29.

What is called subscription received in advance during the accounting year?

(a) An income

(b) An expenditure

(c) An asset

(d) A liability

Answer:

(d) A liability

Question 30.

Which expenditure is shown in Balance Sheet?

(a) Trading

(b) Revenue

(c) Sundry

(d) Deferred revenue

Answer:

(d) Deferred revenue